Heading will come here

View NowMutual Funds

- ICICI Prudential Advisor Series - Dynamic Accrual Plan 31.85 0.00(0.00%)

Equities Indices

Nifty 50

|

10,195.15 10.2600 (-3.3%) 16-03-2018 12:00 |

Prev Close 10,360.15 | Open 10,345.15 | High 10,346.30 | Low 10,180.25 | Details |

Equities

Asian Paints Ltd.(INE021A01026)

| NSE: Asian Paints | BSE: 500820 | Sector: Chemicals |

|

NSE Mar 16 2018, 4:01 1,160.80 23.90(+3.90%) |

BSE Mar 16 2018, 4:01 2,260.90 23.90(+3.90%) |

View Details |

Invest Guide July 2025

India's Capex Story - Will Government and Private Sector Increase Spending in Second Half of FY26?

India's capital expenditure (capex) momentum has regained strength in FY2025-26, following a brief setback in FY25. The first half of FY26 (H1 FY26) showed encouraging signs of recovery, particularly led by public sector outlays. As India progresses into the second half of FY26 (H2 FY26), the key question remains: can the government sustain its momentum, and will the private sector finally catch up?

H1 FY26 - Rebound in Public Investment:

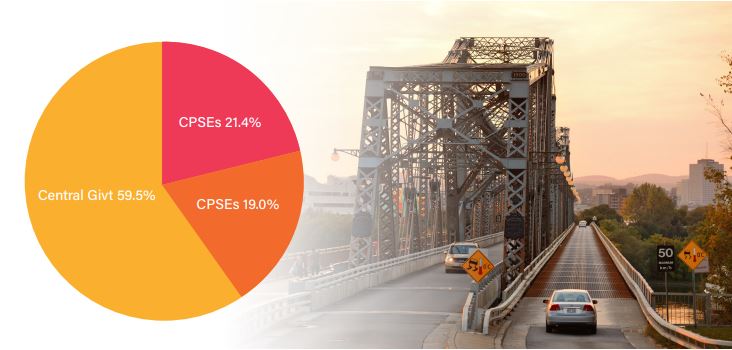

H1 FY26 saw central government capex reach around ₹5.0 lakh crore, nearly 45% of its annual target of ₹11.2 lakh crore, marking a sharp rebound after FY25's sluggish start. State governments contributed an estimated ₹1.6 lakh crore, up around 10% YoY. Central Public Sector Enterprises (CPSEs) spent about ₹1.8 lakh crore in H1, indicating stable execution. Project completion rates improved from the 42% five-year low seen in October 2024.

The uptick stemmed from post-election administrative clarity, better monsoon management, and front-loaded spending. The Ministry of Road Transport and Highways spent over ₹55,000 crore by April 2025, and Indian Railways accelerated work on station redevelopment and Vande Bharat train rollouts. State projects in Maharashtra, Karnataka, and Assam also showed momentum.

Private sector capex, however, remained cautious. After declining 9% in FY25, private investment stabilized in H1 FY26. Green shoots emerged in green energy, electronics manufacturing, telecom, and EVs, but broad-based revival was absent. New project announcements showed slight improvement; execution picked up marginally.

Large corporates continued to prioritize deleveraging and strengthening balance sheets. Capacity utilization in key industries remained below peak levels, dampening the urgency for fresh investments. However, improving demand indicators and easing interest rates could support a more meaningful pick-up in private capex in the coming quarters.

H1 FY26 - Public Capex distribution (lakh crore) -

H2 FY26 Outlook: Government to Sustain Capex Push -

With 45% of budgeted central capex spent in H1, the government aims to deploy the remaining ₹6.2-6.5 lakh crore in H2. Strong tax revenues and RBI dividends offer headroom. Sectoral focus includes:

- Roads & Highways: ₹2.72 lakh crore

- Railways & Metros: ₹2.6 lakh crore

- Defence: ₹1.8 lakh crore

- Telecom & Digital Infra: ₹0.8 lakh crore

- Urban Development: ₹0.6 lakh crore

- Renewable Energy & Power: ₹0.5 lakh crore

Ministries have been directed to maintain quarterly pace, avoid last-quarter rushes, and improve execution. States are tapping the ₹1.5 lakh crore interest-free central loan for capex, with proposals from Uttar Pradesh, Gujarat, and Tamil Nadu leading. States like Maharashtra and Karnataka are expected to post double-digit growth in capex.

CPSEs and States: Execution Will Be Key -

CPSEs have a capex target of ₹7.85 lakh crore in FY26. With H1 stable, H2 is likely to witness the traditional ramp-up. NHAI, NTPC, Rail Vikas Nigam Ltd., and Power Grid have indicated acceleration plans.

States, too, are expected to utilize carry-forward funds from H1 and central loans to boost infrastructure spending. Urban transport, irrigation, and industrial parks will be key areas. Maharashtra, Karnataka, and Assam have already shown progress; states with elections in late 2025 may crowd out capex with welfare spending.

Private Sector Capex: Gradual Revival Expected -

Private capex remains cautious but improving. Key signals:

- Green energy: Solar parks, wind farms, battery storage projects gaining traction.

- Electronics/Semiconductors: PLI-led mobile phone, chip assembly, and display plants under execution.

- Automotive/EV: OEMs investing in EV platforms, batteries, and component ecosystems.

- Telecom/Data Centers: 5G rollouts, hyperscale data parks growing steadily.

Capital goods order books rose ~10% YoY by end-FY25. Manufacturing capacity utilization neared 74% in Q1 FY26, prompting select expansions. However, steel, healthcare, and retail remain muted. FY26 private capex may marginally surpass FY25 levels.

Financing Landscape: More Conducive Than FY25 -

- Bank Credit: Industrial credit up 10.1% YoY (Sep 2025), led by chemicals, power, and engineering. PSU banks active in term lending.

- Corporate Bonds: Q2 FY25 saw 68% YoY jump in issuance; yields now trending lower, aiding infrastructure NBFCs and InvITs.

- FDI: Net inflows stable; electronics, auto, renewable energy attracting new projects.

- Interest Rates: RBI repo rate at 5.5%; potential for further easing if inflation stays within control.

Overall, project financing has become easier due to improving liquidity, lower cost of capital, and investor confidence.

Macro and Policy Environment -

The Union Budget FY26 raised capex allocation by 10%. Fiscal deficit target remains conservative at 4.4% of GDP, emphasizing consolidation with growth. PLI schemes, Gati Shakti, and the National Infrastructure Pipeline provide long-term project pipelines.

Ease of doing business has improved through digitization of approvals, land reforms, and faster environmental clearances. Global realignment of supply chains continues to benefit India under the China+1 strategy.

Opportunities -

- Project execution pickup in H2 with favourable weather

- PLI projects reaching execution stage in electronics, EVs, and solar

- FDI-led industrial clusters gaining momentum (e.g., Gujarat chip plant)

- Crowding-in of private capex due to visible infrastructure rollout

Risks -

- Execution bottlenecks at state/CPSE level due to capacity or admin delays

- Populist state schemes potentially diverting funds from capex

- Global slowdown or oil price spikes pressuring fiscal math

- Commodity price volatility impacting project viability

Conclusion -

India's capex trajectory in FY26 appears resilient. Public sector investments will likely continue to anchor growth, with CPSEs and state governments playing critical roles. Private sector participation remains tentative but is slowly building momentum in high-opportunity sectors.

With favorable financing conditions, policy continuity, and a clear infrastructure vision, H2 FY26 could be a pivotal period for converting intent into investment. If private sector confidence strengthens alongside public efforts, India's capex cycle may enter a durable expansion phase - essential for realizing the vision of a $5 trillion economy by the end of the decade.

Proceed To Complete Registration

Step 1

Personal Details

Step 2

FATCA Details

Step 2

Bank Details

Select Investment Type

Lumpsum

SIP

Equity

Select a scheme to add:

Select a scrip to add: