Heading will come here

View NowMutual Funds

- ICICI Prudential Advisor Series - Dynamic Accrual Plan 31.85 0.00(0.00%)

Equities Indices

Nifty 50

|

10,195.15 10.2600 (-3.3%) 16-03-2018 12:00 |

Prev Close 10,360.15 | Open 10,345.15 | High 10,346.30 | Low 10,180.25 | Details |

Equities

Asian Paints Ltd.(INE021A01026)

| NSE: Asian Paints | BSE: 500820 | Sector: Chemicals |

|

NSE Mar 16 2018, 4:01 1,160.80 23.90(+3.90%) |

BSE Mar 16 2018, 4:01 2,260.90 23.90(+3.90%) |

View Details |

Invest Guide July 2021

InvestGuide July 2021 Edition Is Here -

Market Capitalization

Market Capitalization to GDP Ratio. Are Markets Pricey Or Pricing In Earnings Recovery?

Read More

SEBI's New Rules

SEBI's New Rules Makes REIT(Real Estate Investment Trust) Attractive for Small Investors

Read More

Cryptocurrencies

What are they and should you invest in them?

Read More

Married Women Property Act

The Little Known Arsenal Against Protection From Creditors

Read More

Asset Allocation

What it means for different investors

Read MoreCEO's Desk -

Dear Investors,

Equity markets are again showing upward trends, primarily due to falling number of daily Covid-19 cases and a sharp rise in vaccinations. The key benchmark indices viz. S&P BSE Sensex & CNX Nifty rose by 6% and 7% respectively during the quarter. The mid and small-cap indices outperformed their larger peers with the S&P BSE Mid-cap and S&P BSE Small-cap indices gaining about 12% and 22% respectively during the quarter.

Among sectoral indices BSE Metals and BSE Healthcare were top performers while BSE Realty and BSE Bankex were laggards during the quarter.

Retail inflation based on consumer price index (CPI) rose to six-month high of 6.3% in May, mainly due to rise in food and fuel prices. The inflation number stood at 4.23% in April. The previous high in retail inflation was 6.93% in November 2020.

India's index of industrial production (IIP) rose a whopping 134.44% year-on-year to 126.6 in April due to a very low base in the same month last year. The IIP rose 24.1% year-on-year in March 2021.

Amid coronavirus pandemic, India's gross domestic product (GDP) grew at 1.6% in the January-March quarter of fiscal year 2020-21, but witnessed a contraction of 7.3% for the entire fiscal year.

In June, the RBI's Monetary Policy Committee (MPC) kept the repo rate unchanged at 4 per cent while maintaining an accommodative stance as long as necessary to mitigate the impact of the COVID-19 pandemic. The central bank also announced other liquidity measures to keep the yields contained.

The 10-year Government bond yield has ended the quarter at 6.051%, down by 0.12 bps from the previous quarter. In our view yields are likely to remain range bound till RBI keep on supporting yields. However, with higher inflation and higher commodity prices, debt market yields can come under pressure and gradually inch upwards.

While Covid-19 has impacted economy, there is a sequential improvement as the covid situation gets better and Indian economy unlocks. The government is trying to support the economy through fiscal as well as monetary measures. RBI's Monetary policy has also been extraordinarily accommodative. The economy has shown resilience and is expected to recover in FY22 aided by the fiscal and monetary support, roll out of the covid vaccine and the return of economic activity to pre-pandemic levels except a few sectors. Speedy vaccination drive, large pent-up demand, investment enhancing measures, and better external demand could provide an upside to the growth.

Equity market valuations are currently somewhat stretched, especially from a near term perspective as the markets are forward looking and are running faster than the economic recovery. The key factors to watch out for equity markets going forward are evolving Covid-19 trajectory, the speed and coverage of vaccination drive, corporate earning growth, goverment policy measures and pace of implementation of Govt. reforms measures to revive economy.

We believe that corporate profitability growth should gradually improve due to tighter working capital management, cost control and reduction in interest rate liability. However, the surge in Covid-19 infections, new mutants, subnormal monsoon, higher crude oil and non-oil commodity prices and global financial market volatility have downside risks to the growth.

Overall, we are positive about Indian equity markets from a 3-5 years' perspective. However, in our view, from a valuation and sentiment standpoint the investors need to be a bit cautious in near term considering current rich valuations. Given the sharp run up in recent months, volatility can be expected going ahead.

If you are investing for certain financial goals, you should continue to invest in a staggered manner, regardless of market levels. Sticking to your asset allocations and following a disciplined investment process are the key to reach your financial goals.

Cover Story -

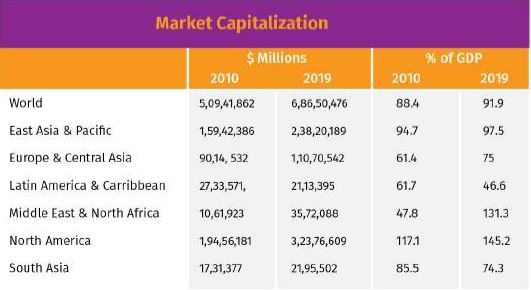

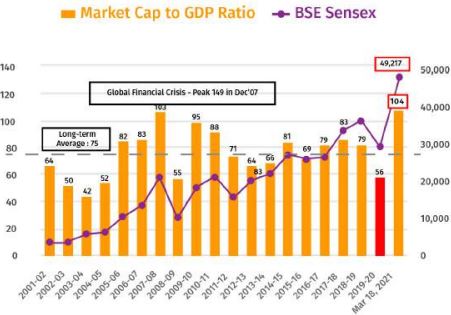

Leaving behind the fundamentals of Macro-Economics, the Indian equity market is touching unseen heights even when the nation's GDP shrank by 7.9% (as per world bank national accounts data) in the financial year 2021 recording its worst-ever performance in the last seven decades. At the end of FY 2021, the market capital of listed companies of India stood at INR 226.5 Trillion which is double of last March. These two figures have resulted in the nation recording its highest Market Capital to GDP Ratio of 104% since December 2007.

The current high Market Capitalization to GDP ratio has raised concerns. Market cap to GDP ratio is a tool used by many investors to estimate and understand the possible direction of the markets. At the zenith of markets in the year 2008, this ratio went up to almost 103 percent for India, and 150% for global markets, being the highest in December 2007. The market experts advise that whenever the ratio (Warren Buffet Indicator) crosses the one there are reasons to be cautious. The Indian markets eventually crashed post 2008 peak and the ratio dropped to almost 55 percent in the FY09.

"...the Indian equity market is touching unseen heights even when the nation's GDP shrank by 7.9% (as per world bank national accounts data) in the financial year 2021 recording its worst-ever performance in the last seven decades."

Know more about Warren Buffet Indicator -

Equating the current listed market capitalization and GDP, it can be deduced that the markets are overheated and expensive at the moment. Before moving forward and analyzing the current scenario, let's understand the Warren Buffet Indicator and learn what it is telling about the Indian Market. Warren Buffet Indicator is probably the best single measure to know where valuations stand at any given moment. It is a model of the total value of all publicly traded stocks in a market divided by that economy's GDP. The ratio above 100 % indicates the market is overvalued and below indicates the market is undervalued (market crash). As of the current Indian market, the ratio stands at 103.56% which is significantly overvalued.

It is one of the finest indicators in the developed country where economic stability can be controlled on par with the national development. When it comes to India this ratio cannot be the only indicator of stock market analysis because of its convergent and divergent economic situations.

"...one needs to understand the concept of ‘Flow' and ‘Stock'. Flows are amounts that are traded per unit. In a financial year, several assets of different values are acquired which is a flow. But the value of an asset that has been bought is a stock. By this definition, we can conclude that Market Capitalization is a Stock and GDP is a flow."

How can value of Market Capitalization be greater than GDP?

Having said that, till now we have understood that the Market Capitalization of common stocks is greater than the GDP of the nation. But, how is it possible? For this one needs to understand the concept of ‘Flow' and ‘Stock'. Flows are amounts that are traded per unit. In a financial year, several assets of different values are acquired which is a flow. But the value of an asset that has been bought is a stock. By this definition, we can conclude that Market Capitalization is a Stock and GDP is a flow. The market cap does not designate the amount bought in the current year, it represents the current value (stock)of certificates accumulated over the years since the company was formed. Investors bought these in the past when they were originally issued. Over time they accrued dividends and experienced price increases. So the value today (a stock) is the result of investments (flows) over years.

Why Market Capitalization of listed companies is compared with GDP?

The answer is straightforward – to assess the health of the stock market. The amount acquired in the stock market of a tiny country like Sri Lanka would be much smaller than the big countries such as China or the USA. In order to scale the stock market, we need something. It can be anything – population size, demography size of the country, etc. In the case of the Warren Buffet Indicator, it's the GDP of the nation. Thus, what people often do is express the size of the market as a percentage of GDP. The countries with relatively larger markets tend to have a better functioning stock market and more liquid stocks.

Returning to the current situation – as mentioned above, the GDP has shrunk but the market Capitalization is booming resulting in widening gap and rising ratio. The Indian Market Capitalization to GDP Ratio has shot up over 100 once again. The market scenario has become a reason of concern for investors. As the indicator states, the markets are over-valued. Why this ratio has become such a huge concern for investors. To comprehend it, we need to turn the pages of history.

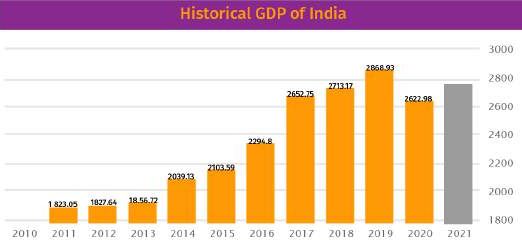

The chart depicts the 10-year GDP of India. India experienced a continuous growth and positive GDP rate till 2020 (global pandemic to be blamed). The nation witnessed GDP of USD 1823.05 Billion in year 2011 which further increased to USD 1827.64 Billion in 2012, USD 1856.72 Billion in 2013, USD 2039.13 Billion in 2014, USD 2103.59 Billion in 2015, USD 2294.8 Billion in 2016, USD 2652.75 Billion in 2017, USD 2713.17 Billion in 2018, USD 2868.95 Billion in 2019. In the beginning of 2020, the nation started struggling with coronavirus resulting in nationwide lockdown from March 2020 onwards. Due to limited economic activities, the country recorded negative growth of worth USD 2622.98 Billion in 2020.

The GDP of India was worth USD 2622.98 billion dollars in 2020 after encountering a negative growth rate of 7.3%. In light of pandemic, the economists projected a contraction of 8% for India. The nation performed marginally better than the projected adversity. Prior to COVID pandemic, India recorded GDP growth rate of 4%. In year 2018, the nation recorded highest GDP worth USD 2868.93 billion.

The first quarter report of FY 2021 has arrived where the nation's GDP expanded 1.6%. The COVID situation is improving with the increase in number of successful vaccinations. In consideration of current circumstances the analysts forecast that Asia's 3rd largest economy is expected to grow at world's fastest rate.

In spite of encountering the growth bump of the nation due to the second wave of COVID in India, the stock market of the nation is flourishing like there's no tomorrow. The given chart depicts the 16-year growth of India. India's Market Capitalization has grown at a CAGR of around 18 percent in the past two decades. India has ranked at 8th position in terms of Global Market Capital with its USD 3 trillion capitalization.

Talking about achieving a significant milestone of USD 3-Trillion Market Capital, there are some interesting figures that the market capitalization history of India holds for us. The nation took 70 years since Independence to reach the market capitalization of USD 1-Trillion in 2007. Then, it took 10 years to double the previous capitalization and touch the milestone of USD 2- Trillion in 2017. And now the country has attained its USD 3-Trillion mark in 2021.

Historical Ratio of Total Market Capital over GDP of India -

Market Capitalization to GDP Ratio which is also known as Buffett Indicator is calculated by taking the sum of listed stock market capitalization and dividing the same by Gross Domestic Product. Warren Buffett described this indicator as best measure in his December 2001 Fortune Magazine article. Market Capitalization to GDP ratio keeps a check on the valuation and sentiment of any market. Any movement above or below hundred indicates the investor whether the market is undervalued or overvalued.

Taking a peek at the history, the Buffett Indicator has rarely exceeded 100 but this is not the first time when the ratio has gone above hundred in India. The remarkable years in Indian Stock Market – 2007, 2017 and 2021, the years when the market capitalization crossed USD 1 Trillion, USD 2 Trillion and USD 3 Trillion mark, were the same years when the indicator crossed 1. It must be noticed that in past two scenarios – 2007 and 2017, markets corrected. And this can happen again as well.

The long-term average of Market Capitalization to GDP is around 0.75x whereas the current ratio is around 1.1x. Further, in the developed countries such as USA, the ratio ranges between 1.4x to 1.8x.

Global Comparison -

As of today, the total market index stands at USD 45563.4 Billion which is 206.5% of the latest reported GDP. Taking world market capitalization into consideration, the stock market recorded two peaks in Market Capital/GDP Ratio– in year 1999 and 2007. In year 1999, the boom of technology came to an end and in year 2007, the global markets suffered financial crisis caused by subprime mortgage crisis. At this point, the developing nation like India also encountered its highest Market Capitalization to GDP Ratio ever – touching the peak of 146%.

Taking into consideration the BRICS countries (Brazil, Russia, India, China and South Africa), India has recorded the highest ratio (excluding South Africa). China's current ratio stands at 81%, 52% in Russia and 73% in Brazil. India share similar per capita income with Indonesia and the ratio over there is around 47%.

Key-Points of Market Capitalization to GDP Ratio Chart -

Different opinions are prevailing in the market. Some investors believe that this is just temporary or India's step towards development. And some cautious investors are considering the past records and believe what Buffett indicator theoretically stands for. As per a report by Motilal Oswal Finance Services, there are certain key-takeaways that must not be ignored by a careful investor.

The GDP growth rate of an economy ultimately settles at less than 6% after attaining a rate of 7%-8%. India suffered multiple lockdowns due to global pandemic just like other countries. It can be concluded that the economy is at the edge of revival. Once the businesses start running at full pace, the GDP will grow at remarkable rates resulting in deflation of the mentioned ratio.

An important factor towards shooting of Market Capitalization can be IPOs. In year 2017, the markets accounted collection of USD 12.5 Trillion which is further not added in GDP. Same can be the scenario here as well. IPOs become a part of market capitalization without actually interfering with the gross domestic product of the nation.

Over the past few years, with the emergence of technology and digitization the recording and analysis of data has become feasible. Now, the companies can't hide the real figures of sales and income resulting in more transparency. With passing years, a more clearer picture of GDP can be expected.

Is it a bubble?

In stock market, a bubble is generally referred to a situation when the price of an individual stock or a financial asset or class of assets is overvalued resulting in excessive worth that its fundamental value.

India's Market Capitalization is much higher than the long-term average of 77% but still much lower than the peak of 2007 boom recorded at 149%. Another notable data figure with NSDL – FPIs (Foreign Portfolio Investors) pumped in INR 14,750 crore in Indian economy in January so far. Till now, this can be understood regarding current scenario of Indian market that the liquidity boost, foreign fund inflows and corporate earnings are pushing the market high. In consideration of these factors, the analysts have raised their suspicions over the rich valuation of the market. Experts believe that a lot of stocks are in the bubble. Also, the market will encounter correction. But there are certain points that you must not miss.

Market Capitalization changes every day but the GDP numbers are declared once in a year and that too with a lag. Year 2020 encountered negative growth and even year 2021 faced lock down. By year 2022, we can expect that the situation will improve resulting in better production, more employment opportunities and stable economy. In light of these factors we can expect a better number of GDP which would ultimately affect the ratio.

Conclusion -

Market Cap to GDP ratio is an absolute method of assessing whether the stock markets are overpriced or not. However, we should be a little more cautious of the numbers in an developing economy like India where we still are taking steps towards more organized business and sector.

SEBI's Rules for REIT -

India's commercial real estate market has been on the upswing. The average tenancy has gone up to 90%. and this has been backed by a good occupancy rates. This has improved cash flow visibility. Global Private Equity funds (PE) have been steadily pouring money in REITs. It can be safely assumed that over the period of a few years decent capital appreciation can be seen in “A” grade properties.

It is interesting to note that top 10 developers and funds hold the portfolio of 180 million square feet (msf) which translates into annual rental income of more than Rs. 16,000 crore. The REIT is fast gaining popularity and it has the potential to raise more than Rs. 1 lakh crore in investments.

Why sudden surge of interest in REIT?

The investment in residential property is on decline because of limited capital appreciation scope, and inability of assets to get monetized. REITs, on the other hand, work like a mutual fund. It invests in income-yielding real estates. REITs can be listed and traded on stock exchanges. This provides investors an opportunity to invest and divest in portfolio instead of physical asset. Thus, an investor with the time frame of 5-7 years need not worry about the liquidity of his investments.

REIT is a win-win proposition for all. The developers get access to investments which can be used to reduce debt and fund construction activities. This in turn will improve their credit profile.

"Things are changing now. The rules have been modified in an attempt to make REIT more attractive for developers and investors alike. However, one must remember that the compliance requirements for REITs is very high."

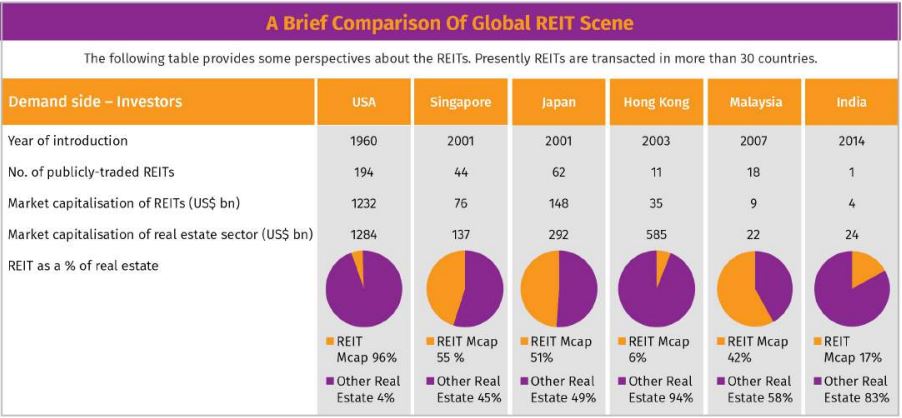

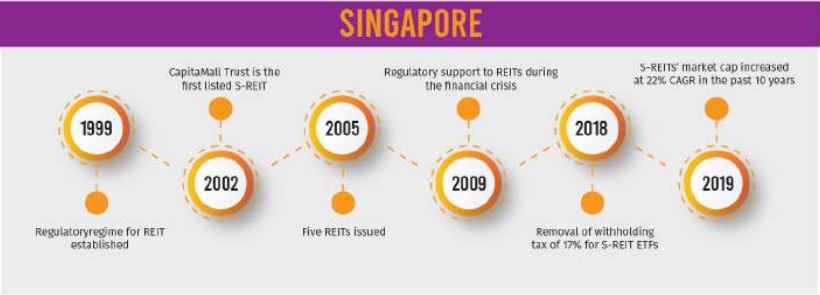

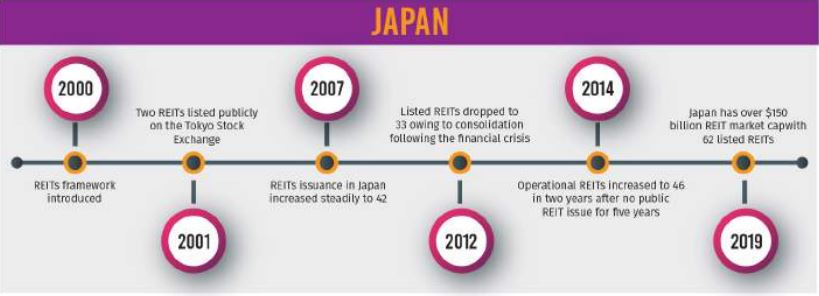

In Singapore and Japan, REITs account for nearly 75% of the asset monetization in real esttae sector. USA, which pioneered the concept of REIT, account for nearly 95% of the asset capitalization. There seems to be huge potential in India due to its vast market size. However, India is facing hurdles in the form of regulatory support and lack of incentives that is hindering the growth of the market.

Things are changing now. The rules have been modified in an attempt to make REIT more attractive for developers and investors alike. However, one must remember that the compliance requirements for REITs is very high. This has been a discouraging factor for smaller developers who would not dilute their stake. The small developers continue to prefer the traditional route of lease rental discounting loans which are cheaper.

In India, the real estate sector can be divided into two spectrum, residential and commercial. The aim of commercial real estate is generate adequate returns through rental income. Commercial real estate includes office, retail, industrial and hotels.

The trend is changing for positive. Developers have begun exploring the alternative route of funding in an attempt to deleverage their balance sheets. If we see the trend, in the past there years, nearly Rs. 70,000 crore has been parked in commercial real estate.

Understanding REIT -

Real Estate Investment Trust (REIT) is a corporation that finance real estate across range of sectors. Basically, the assets held in the Special Purpose Vehicle (SPV) are transferred to the REIT in lieu of the units. The SPV manages the assets. Tenants pay rent to the SPV which subsequently flow to the REIT. Similar to mutual funds, the unit holders receive dividend which is net distributable income of the REIT.

The Property Scene In India -

As mentioned before, Indian REIT scene holds promise for investors. Around 180 msf of assets can be monetized. However, this would also result in significant stake dilution on the part of developers.

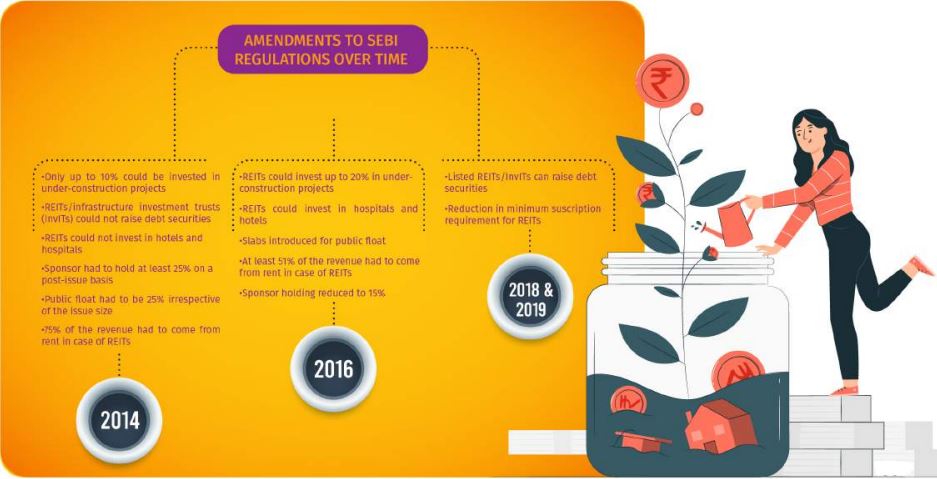

SEBI introduced REIT in India in 2014. However, due to regulatory framework the concept of REIT failed to take-off from ground. The first issue by Embassy Property Development Pvt Ltd hit the markets only in 2019, five years after REIT was introduced. SEBI's original REIT regulations has undergone several changes and amendments.

In India, the first REIT was issued by BRE Mauritius Investments and Embassy Property development Pvt. Ltd. The issue hit the market in 2019 and was oversubscribed. The REIT was successful in beating the benchmark S&P BSE Realty in terms of returns.

Embassy Office Parks REIT has 11 commercial assets, hotels and a solar plant.

USA has the highest number of publicly traded REITs followed by Japan and Singapore. India has only one publicly traded REIT. In USA, the market capitalization of REIT stands at US $ 1232 billion while in India it is merely US$ 4 billion. Hong Kong too have only 11 publicly traded REITs. The low number of REITs can be attributed to lack of incentives or regulatory support. Hence, a good regulatory framework that provides incentives to the developers and investors can go a long way in developing the market for REIT.

India is not alone in the sluggish progress made by REIT. Even in USA, the pioneer of REIT, it took several decades for investors to embrace the idea of investing in REIT.

Are REIT Safe As Investment Instruments?

REITs can be a blessing in disguise for investors who find it difficult to invest in commercial real estate due to prohibitive costs. The residential market is struggling with negligible returns.

REITs provide assured return to investors since the dividend has to be distributed compulsorily. Presently around 90% dividend has to be distributed among the unit-holders. Investors can also benefit from the improved valuation of the assets under management. Further, REITs have stringent regulatory and compliance network making it extremely safe for investors.

In June 2021, SEBI relaxed investment norms in REITs. Small investors could not participate in real estate sector due to high entry costs. SEBI has lowered the minimum application value for Real Estate Investment Trusts (REITs) from Rs 50,000 to Rs 10,000 to 15,000, a move that is expected to make the market more accessible to small and retail investors. This will expand the retail participation and pave way for listings.

The earlier cap of Rs 50,000 was very prohibitive for small investors. Currently, there are three public listed office REITs in the country – Embassy REIT, Mindspace Business Parks REIT and the most recently listed Brookfield India REIT.

What makes REIT attractive for small investors?

In an uncertain investment world, REITs offer handy option to generate decent returns. A Real Estate Investment Trust can be launched only if 80% of the underlying assets are operational and income generating. Thus, the investor need not worry about operational uncertainties while investing in REIT.

The COVID pandemic did batter real estate sector, but things are beginning to look brighter now. The commercial real estate market has always been profitable proposition. More than 60% of the A grade property is REIT-able. It is expected that in the coming years more than 100 million square feet property will be listed on stock exchanges. Due to pandemic, the commercial real estate might experience some pressure on rentals, but if one is to consider broader picture, the sector is considered as resilient and low risk. India is fast becoming global IT outsourcing place, and with time, the commercial real estate sector is expected to deliver high returns.

The property market is set to witness hectic activity in the coming years. The government's thrust to monetize the assets of the PSUs will provide further fillip to real estate sector. Naturally, the government will be looking at REIT/Investment Trusts as a viable option.

With ticket size reduced to Rs. 10,000 - Rs. 15,000 per unit, the REITs have become attractive investment proposition for small investors. This will also enable better liquidity and price discovery mechanism which will eventually benefit small investors.

Cryptocurrencies: Should You Invest?

"Cryptocurrencies has hogged attention of investors. Though risky, the phenomenal returns witnessed in past few years have made them hot commodities. But every coin have two sides."

What is a cryptocurrency?

Cryptocurrencies have to be mined. In simple terms, coin mining is a method of calculating the value of cryptocurrency assets through a cryptographic process. These processes mine coins in blocks, which are simply ledger files that permanently record all recent cryptocurrency transactions. It has been called mining because the individuals who get new coins earn it in small and finite quantities periodically, similar to gold.

As for the negative side, since, cryptocurrencies are digital, they are vulnerable to hackers who indulge in criminal activity. A security breach can mean huge loss to the investor. Though, measures are taken to protect investor's interests, they have not been extensively tested in real world. The positive version being cryptocurrencies help to diversify one's portfolio. A person can utilize them as a mode of payment worldwide. The payment mechanism through cryptocurrencies can potentially save a lot of money in fees and charges.

However, the fact remains that despite the growing popularity of cryptocurrencies, many investors are hesitant to invest in a booming cryptocurrency market.

Investing in cryptocurrency sounds more like a game of luck. The volatile movements defy the traditional conventions of investment. It is to be noted that in India, cryptocurrency transactions are just fraction of what they are globally.

The confusion around cryptocurrencies stem from the fact that they are still viewed as emerging commodity that is backed by a fraction of investors. Unlike equities or commodities, they lack wider acceptance. From the pure risk point of view, they are no different than traditional products, in fact, they are perceived as more risky and volatile due to wide-spread opposition worldwide.

In a country like India, the laws on cryptocurrency are unclear. The lack of regulation is the biggest hurdle in cryptocurrency investing. It must be noted that in 2018, RBI issued a blanket ban of trading or dealing in cryptocurrencies. Given RBI's stand, even if one invests in cryptocurrency, there is a risk of remittance and accounting that could jeopardize one's capital. Though, RBI's circular was set aside by Supreme Court in 2020, banks are hesitant to deal in cryptocurrencies.

The government's stand on cryptocurrencies is the biggest risk for its investors. Until now, the government has remained silent, but should the government decide to ban cryptocurrencies, the investors could face heavy losses.

Recently, there were reports that many cryptocurrency owners had hard time retrieving their accounts due to forgotten passwords. In case, if the investor forgets his wallet password or his account get hacked, he is at permanent loss. Unlike shares and commodities, cryptocurrencies do not enjoy the protection of insurance. They are not accepted at merchant outlets and more importantly it is difficult to determine its store value. All these could be scary for a investor who is familiar using traditional tools to analyze risk-reward in investments.

The younger generation seems to be obsessed with the idea of cryptocurrencies. The technology behind cryptocurrencies is still at nascent stage which makes investing a pure gamble of luck. The backers of cryptocurrencies argue that they are futuristic commodities which will be embraced sooner or later.

Understanding The Process Of Cryptocurrency -

Mining :

Mining is an activity where an individual (called the “miner”) uses his computer prowess to crack computationally difficult puzzles. The process of cracking such puzzles which are integral to the blockchain technology, help in maintaining them. As a reward for this, the miner gets new bitcoins which is nothing but creation of a bitcoin or mining.

Purchasing them from a bitcoin exchange against real currency :

Everyone cannot be a bitcoin miner. Hence, you can consider buying bitcoins from bitcoin exchanges and store them in an online bitcoin wallet in digital form. Unicorn, Bitxoxo, Zebpay, Coinbase etc., are some of the bitcoin exchanges presently in India. Such bitcoins would be purchased in consideration for real currency.

Receiving bitcoins in consideration of selling goods and services :

Though this may not be a common phenomenon in India currently, there are a few savvy businessmen who accept bitcoins (instead of real currency) on sale of goods or services, they deal in.

Cryptocurrencies Returns :

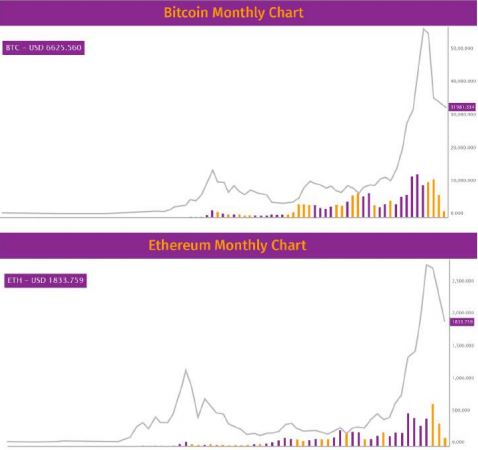

The following is the monthly chart of Bitcoin. Till February 2017, the price of one Bitcoin hovered around $1100. By April 2021, the price skyrocketed to $64000. This does not mean that Bitcoin consistently delivers such performance. After hitting $64000 in April 2021, in next two months, the price of Bitcoin crashed by 50%. Investors who invested at the beginning of 2021 are staring at huge losses. The same can be said of other cryptocurrencies like Ethereum or Tether.

Taxation of cryptocurrencies :

Cryptocurrencies are considered as digital money. Litecoin, Ethereum, Zcash, Dash, Ripple etc. are some of the cryptocurrencies that are popular in India. In India, the money is regulated by RBI, but as stated before, RBI has sought to ban dealing/trading in cryptocurrencies. The government too has not brought any legislation to regulate them. Hence, statutorily cryptocurrencies cannot be taxed, at the same time, Indian tax laws have always sought to tax income received irrespective of the form in which it is received.

Tax Implications On Miners :

If a person is mining a cryptocurrency, say Bitcoin, he is generating a capital asset. In ordinary circumstances, such action on any form of assets is liable for capital gains. However, in case of Bitcoin, it is difficult to determine acquisition cost since it is a self-generated asset. Section 55 of the Income Tax Act states that where the capital assets has become property of the assessee before 01.04.1981, then the cost of acquisition of such an asset will be the actual cost to the assessee or fair market value as on 01.04.1981 at the option of the assessee. In case of cryptocurrency mining the capital gains computation mechanism fails. Technically, no gapital gains tax would arise for cryptocurrency mining. In the absence of laws, it depends upon the Income Tax authority whether to consider cryptocurrencies capital asset as all or whether to tax them under income received from other sources.

The Indian government is considering the Cryptocurrency and Regulation of Official Digital Currency Bill, 2021, which could ban all private cryptocurrencies in India. Thus, it can be concluded that Indian investors who are enthusiastic about investing in cryptocurrencies are playing with the fire.

How To Trade Cryptocurrency In India :

Getting started with cryptocurrencies can be daunting and may require a thorough understanding of this virtual currency and the factors that affect its value. However, certain exchanges make it very simple for enthusiasts and serious players to trade in these currencies. Crypto Exchanges are online platforms that make it simple for those unfamiliar with trading in this asset class. One of the most popular exchanges in India is WazirX.

WazirX's app is one of the most popular cryptocurrency trading apps among Indian investors. This Exchange also offers its native utility token, WRX, that can be bought with the Indian rupee and invested in various cryptocurrencies.

MWP Act -

Not many people have heard about Married Women Property Act. This act is very important from a personal finance perspective. Even if one searches the internet, the only reference one can find relates to Section 6 of the Act, which reads as, “a policy of insurance effected by any married man on his own life and expressed on the face of it to be for the benefit of his wife, or of his wife and children, or any of them, shall ensure and be deemed to be a trust for the benefit of his wife, or of his wife and children, or any of them according to the interests so expressed, and shall not, so long as any object of the trust remains, be subject to the control of the husband, or to his creditors, or form part of his estate.”

This is one of the most powerful act that protects the interest and rights of a women. Married women property act is 142 years old act. It was formulated in 1874.

Why should one take the policy under the married women property act?

There are certain provisions of the insurance act, 1938 which deal with assignment and nomination of the life insurance policies. Before the insurance act was enacted, the general practice was that the person to whom the payment was to be made under the policy had to get a succession certificate or letters of administration to prove his rights. Right did not exist by the mere mention of his name being mentioned in the policy. Section 38 of the insurance act deals with the assignment and transfer of life insurance policy. Under this section the policy can be assigned only after attestation by at least one witness. However search assignment is effectual between the parties but not against the insurer. In order for the assignment to become effectual against the insurance it is also necessary to give the written notice of the transfer or assignment to the insurance while completing the formalities as provided in section 38 (2) of the act.

However if the policy is issued under section 6 of the married women's property act then the nomination under section 39 of the insurance act would not apply. It means that in case of dispute between the beneficiary and the nominee the beneficiary registered under the married women property act well receive the the benefits of the policy.

Let us understand some of the provisions of married women property act.

The debt of the married woman before marriage is the liability of the husband. For example if the wife has taken an education loan before marriage then after marriage the loan becomes the liability of the husband. There is no provision in the act to file any claim against such debts.

However the state governments have been given power to amend the provisions of the act. Hence the rules maybe different from state to state.

The following assets are classified as Streedhan or separate property of the women. It is to be noted that the husband has no right whatsoever on the following assets:

- The salary or any kind of income before or after marriage is considered as Streedhan. Such income could be the result of employment or a business.

- Any income arising from her artistic skills.

- Any savings or investment which is done from the aforementioned income is considered as Streedhan.

- If the women purchase insurance policy before marriage then the benefits of such policy is considered as the separate property of the women.

It is to be noted that as per married women property act if the women shares her separate property as explained above with her husband then she can always recover the same through legal proceedings as it is considered as Streedhan.

Let us understand the impact of insurance policy under section 6 of married women property act :

Many times it happens that a person has an ongoing home loan or has incurred debts in a business. In the event of the death of a person the sum assured can be claimed by the creditors attached by the court for repayment of his debts. In such a scenario the person's wife and children may not get even a single rupee from the surrender of the policy. This situation can be avoided by purchasing the life insurance policy under the married women's property act, 1874.

The following scenarios explains how purchasing the policy under the married women property act is beneficial :

People are of misconception that with the death of a person his debts are waived off. Generally the creditors can recover the debt from the insurance proceeds of the deceased. However this can only be accomplished through the court orders. Hence if one purchase the policy under section 6 of married women property act then he can protect the interests of family members after his death.

Many times there are certain circumstances where a married woman might want the insurance proceeds to be passed to her children after her death. Purchasing the insurance policy under section 6 of the married women's property act enables her to do so. This can be done by appointing the children as beneficiaries. For example, If the woman has two children she can assign specific percentage of the sum assured to each beneficiary. However, once the policy has been issued, the beneficiaries cannot be changed. In case a person wishes to change the beneficiary he has to obtain the consent of the beneficiary.

Who can opt for insurance under the married women property act?

Any person who is a resident of India and married can purchase the insurance policy under the married women property act. One should know that it is not possible to convert existing policy under married women property act. The insurance policy can be covered under this act only at the time of purchasing the policy. One can find the option to get the policy covered under this act in the proposal form.

Since the policy does not belong to the policyholder he cannot avail loan against the policy once it is issued under this act.

What if the woman has offered a personal guarantee for any kind of loan?

If the woman has offered any form of personal guarantee for any credit or loan then the provisions of this act would not be applicable. Even if the woman has taken out a loan and if she defaults then too she cannot claim immunity under this act.

How to take an insurance policy under the married women protection act?

The process of getting insurance under the married women protection act is very simple. All a person needs to do is to tick the box in the proposal form or attach an addendum along with insurance application at the time of taking the policy.

Asset Allocation

Asset allocation is an integral part of investing. It helps the investor to meet his financial goals quite efficiently.

It is a common knowledge that diversification is the key to success of a portfolio. However, even a diversified portfolio can send investment goals out of whack if it is not properly tracked.

There is no easy answer as to how frequently portfolio should be re-balanced. However, long term investors can re-balance their portfolio once a year. There is a notion that in order to re-balance one's portfolio, one must track the markets on a daily basis. This is not true. In fact, if you track your portfolio everyday it will generate a lot of noise and distort long-term picture.

While undertaking asset allocation one must remember that gains, if any, are taxed. For example, for equity mutual funds, the short term capital gain is taxed at 15%, while long term capital gain is taxed at 10% (if held for more than a year).

"Long term investors can re-balance their portfolio once a year. There is a notion that in order to re-balance one's portfolio, one must track the markets on a daily basis."

The Puzzle Of How Much To Allocate

Traditional advisors have been advising to allocate in the ratio of 50:50, i.e. 50% equity and 50% debt. Here too, if we consider tax implications, then the asset allocation should be in the ratio of 65:35.

But this might not work for everyone:

For one, for someone in 30s, being time on their side is highly advantageous. It is a common knowledge that returns smoothen over long period. Let's say you invested Rs 5,000 every month in Kotak Blue Chip Fund, then even after considering big crashes of the year 2000 and 2008, your absolute returns would have been 74%. In short, by investing just Rs. 5,000 every month, you would have still accumulated Rs 23 lakh.

But if someone is in his 50s, the two big crash of 2000 and 2008 would have resulted in loss of returns and hence he would be staring at negligible returns a decade later.

What is The Best Asset Allocation Strategy?

The best asset allocation strategy is the one which compliments your risk profile. The criteria for asset allocation is the maximum loss that an investor can suffer without panicking. Let's review some popular asset allocation strategies.

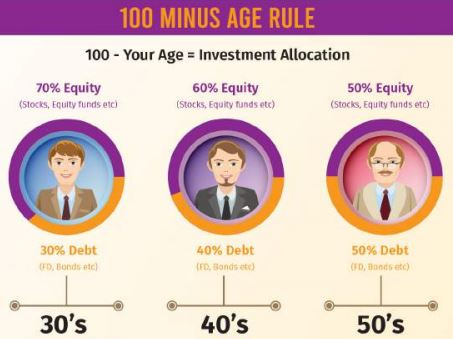

Age Based Asset Allocation -

The rule of 100 is extremely popular among investors to gauge their asset allocation. This rule is quite effective. It accurately tells an investor how he should invest his money. For example, if the investor is 25 years old, then as per the rule of 100, his asset allocation will look like:

100 - 25 = 75

Thus, 75% amount should be invested in equities and 25% should be invested in debt.

Similarly, for someone approaching retirement at the age of 60, the asset allocation would be:

100 - 60 = 40

Thus, 40% should be invested in equity and remaining amount should be invested in fixed income products.

This conventional model is extremely simple, and highly effective.

The Good Old 50:50 Ratio -

If you are a new investor you can follow 50:50 based asset allocation strategy. This too is very effective from returns point of view. Even balanced funds work more or less on the same principle. This model works well for conservative investors. If the investor thinks that the markets are overpriced, he can allocate more assets towards fixed income products. Similarly, if the investor thinks the markets are underpriced, he can allocate more money to equities.

Ideally, how much to allocate to equities or debt depends upon the risk profile of the investor.

An Asset Allocation Strategy For Senior Citizens -

Let's assume a person is nearing retirement or is already retired. Assuming the retirement age at 60, a person needs to plan for at least 30 years of his remaining life. If the person's annual expenses are Rs. 8 lakh, then he is required to invest past 15 years of his expenses in fixed income products, i.e. in this case Rs. 1.8 crore (Rs 8 lakh x 15). If he puts the money in low risk short duration fund, since these funds deliver returns that can match inflation, This strategy allows the investor to withdraw money at monthly or quarterly interval to meet his inflation adjusted expenses.

Even though this strategy quite stress-free, still it covers only 15 years of post-retirement life. Still the investor need to plan for his remaining years. Here, he invests 3-4 years of his expenses in lumpsum in equity funds and let it sit idle for 15 years. If he does not withdraw money for 15 years, the money will compound itself which can offer him protection in his post-retirement years.

This asset allocation strategy is very useful because the investor does not depend upon equity funds to meet his expenses. This also enables his corpus to grow faster due to the effect of compounding.

How Often Should You Do Asset Re-Balancing -

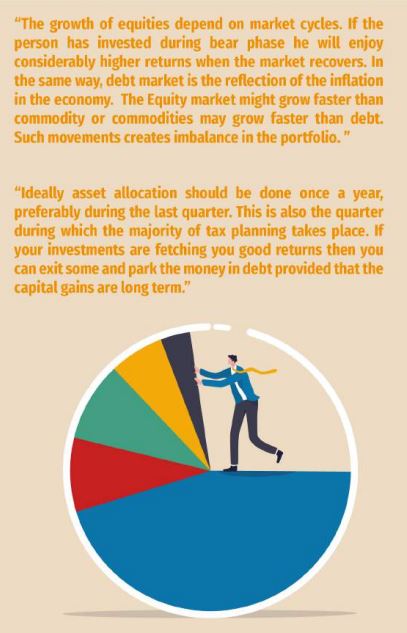

The growth of equities depend on market cycles. If the person has invested during bear phase he will enjoy considerably higher returns when the market recovers. In the same way, debt market is the reflection of the inflation in the economy. The Equity market might grow faster than commodity or commodities may grow faster than debt. Such movements creates imbalance in the portfolio.

Asset allocation depends upon the risk profile of the investor. Suppose an investor wants to distribute his assets as following:

- 50% for equities

- 30% for debt

- 10% for commodities

- 10% International markets

Now, in the bull market, when the price of equities rise, his asset allocation might suffer some imbalance. The rise in equity prices globally can skew his portfolio to:

- 55% equities

- 22% debt

- 11% commodities

- 12% International markets

Clearly, he has to re-balance by shifting some portion of his equity to debt to achieve optimum allocation.

Ideally asset allocation should be done once a year, preferably during the last quarter. This is also the quarter during which the majority of tax planning takes place. If your investments are fetching you good returns then you can exit some and park the money in debt provided that the capital gains are long term.

What Is Considered As An Asset?

Almost every investor has some form of gold or old stocks or even collectibles like coins or investment in government schemes like PPF.

Even while considering the investment plan, many investors fail to disclose all assets to their financial advisor. This distorts the picture and results in erroneous planning. If someone has a plot of land, he might not have idea of its valuation. There are instances of investors inheriting shares in physical form only to forget about them later due to unawareness of converting it in the demat form.

Sometimes people do not remember all their investments. This prohibits them from getting an holistic view about their portfolio which leads to poor financial planning. It is not that investors deliberately forget about their assets. Many times they do not consider the inherited assets as investments as all.

Many do not even have an idea what is an asset. In economic parlance, anything that can be liquidated can be called as asset or investment. Self-occupied property which is used for residential purposes cannot be counted as an asset, but a second house or a second property received from inheritance should form part of asset while planning asset allocation.

Conclusion :

Asset allocation can prove to be tricky in absence of complete facts and figures. Even then, it might be difficult for an investor to decide on asset allocation on assumption of his risk profile. It is highly advisable to consult one's financial advisor to get a holistic view of one's portfolio.

Media -

"InvestOnline strives to share knowledge and actionable strategies to manage money smartly. Read our blogs and latest articles to gain valuable insights in the world of finance."

Why Thematic Funds Like Commodities Deserve Asset Allocation?

Before the pandemic the demand for commodities saw deflationary pressures. The commodity stocks underperformed the market. This was not a local problem, the situation was the same across the globe. This was evident from the purchasemanagers index (PMI) for industrial production which spiralled downwards for few...

Read More

VAX AND VIGIL FOR YOUR ASSETS

Many were afraid to buy during corrections due to high volatility. But with volatility subsiding, those who were waiting on the sidelines have jumped the bull bandwagon. Investors realized that the longer they wait, the more they will miss out on dividends and growth. The underperformance of the debt funds...

Read More

COVID-19 Pandemic: How To Manage Health Insurance And Emergency Funds?

The pandemic has been hard on world economies. Every country is fighting a battle to beat the virus and minimize the damage to its economy. As far as personal finance is concerned one should remember that things could go haywire and it pays to be prepared. Building a emergency fund and having adequate...

Read More

What Is Emergency And Why You Need Emergency Fund?

Life is uncertain and we should be financially prepared for all sorts of uncertainties. Having a sufficient amount of money for the uncertainties not only allows us to handle an emergency, but empowers us to lead a financially carefree life and focus on long-term investments as well...

Read More

Abhinav Angirish Talks About Entrepreneurship Challenges

Abhinav Angirish Talks About Entrepreneurship Challenges & What Makes The Entrepreneur Successful...

Read MoreMarket Update

Fund Performance - Large Cap

| 1yr | 2yr | 3yr | 5yr | 7yr | 10yr | |

|---|---|---|---|---|---|---|

| KOTAK BLUECHIP FUND (G) | 56.01 | 19.87 | 15.82 | 13.90 | 13.36 | 12.69 |

| PGIM INDIA LARGE CAP FUND REG (G) | 53.28 | 15.93 | 13.39 | 12.55 | 12.10 | 11.79 |

| IDFC LARGE CAP FUND REG (G) | 46.98 | 15.96 | 12.18 | 13.24 | 10.43 | 10.65 |

| CANARA ROBECO BLUECHIP EQUITY FUND (G) | 50.87 | 21.99 | 17.96 | 16.80 | 13.82 | 13.65 |

| BNP PARIBAS LARGE CAP FUND (G) | 44.96 | 17.34 | 14.89 | 13.00 | 12.62 | 13.98 |

Fund Performance - Mid Cap

| 1yr | 2yr | 3yr | 5yr | 7yr | 10yr | |

|---|---|---|---|---|---|---|

| AXIS MIDCAP FUND (G) | 62.16 | 28.65 | 21.42 | 19.32 | 16.86 | 19.29 |

| PGIM INDIA MID CAP OPP FUND REG (G) | 100.00 | 42.48 | 23.84 | 19.14 | 16.45 | - |

| BNP PARIBAS MID CAP FUND (G) | 75.28 | 28.77 | 19.05 | 15.02 | 16.16 | 18.54 |

| CANARA ROBECO EMERGING EQUITIES REG (G) | 64.91 | 23.64 | 16.65 | 17.93 | 18.71 | 20.20 |

| EDELWEISS MID CAP FUND REG (G) | 87.51 | 30.35 | 18.47 | 17.93 | 17.82 | 19.20 |

Fund Performance - Small Cap

| 1yr | 2yr | 3yr | 5yr | 7yr | 10yr | |

|---|---|---|---|---|---|---|

| QUANT SMALL CAP FUND (G) | 181.62 | 59.45 | 31.42 | 20.20 | 17.05 | 14.60 |

| KOTAK SMALLCAP FUND (G) | 119.51 | 40.21 | 23.92 | 19.73 | 19.89 | 18.74 |

| CANARA ROBECO SMALL CAP FUND REG (G) | 105.56 | 37.43 | - | - | - | - |

| EDELWEISS SMALL CAP FUND (G) | 105.82 | 37.72 | - | - | - | - |

Fund Performance - Tax Saving

| 1yr | 2yr | 3yr | 5yr | 7yr | 10yr | |

|---|---|---|---|---|---|---|

| IDFC TAX ADVANTAGE REG (G) | 83.30 | 22.75 | 15.25 | 16.96 | 15.69 | 16.01 |

| QUANT TAX PLAN (G) | 113.46 | 43.04 | 29.88 | 22.88 | 23.70 | 15.49 |

| PGIM INDIA LONG TERM EQUITY FUND REGULAR (G) | 61.84 | 19.43 | 14.64 | 14.84 | - | - |

| CANARA ROBECO EQUITY TAXSAVER FUND REG (G) | 65.10 | 24.28 | 20.36 | 17.91 | 14.95 | 14.75 |

| BNP PARIBAS LONG TERM EQUITY FUND (G) | 47.52 | 18.46 | 14.84 | 12.77 | 12.89 | 14.46 |

Proceed To Complete Registration

Step 1

Personal Details

Step 2

FATCA Details

Step 2

Bank Details

Select Investment Type

Lumpsum

SIP

Equity

Select a scheme to add:

Select a scrip to add: