The NBFC crisis and the then-unprecedented Covid-19 outbreak were just two of the economic crises that the Indian economy experienced over the course of the last four fiscal years. The epidemic, which manifested itself in three waves, lasted for about two years and continuously harmed the economy's hopes for recovery.

But now that the pandemic seems to be over, attention is turning to getting each country's economy back on the path of healthy growth. Their attempts have been restrained, nevertheless, by the evolving geopolitical environment brought on by the current Russia-Ukraine conflict. Its knock-on effects have caused many enterprises to adopt a cautious approach across several geographies, raising concerns about an impending economic crisis.

The Indian economy, which reported growth of 8.7% in FY22, stands out as one of the exceptions to all of this, demonstrating significant signs of a comeback. Based on the groundwork that was laid over the past several fiscal years to empower stakeholders, support the banking and financial services sector, increase transparency, and most crucially, launch the largest Covid immunisation programme in the world, it is anticipated that this growth will signal the start of a time of sustainable growth.

The committed government of India worked in tandem with a perceptive and flexible regulatory framework to protect and steer the economy through the difficult period. When the initial challenges subsided, the Indian financial authorities are now adjusting to the futuristic demands of efficient financial technology use and rising sensitivity to the ESG factors in the financial markets.

As a result, India is currently experiencing a protracted and paradigm-altering growth era. It will be interesting to see how the economy develops going forward. India's economy is currently the fifth largest in the world, but it appears to be on a development trajectory that will eventually see it rank among the top three economies.

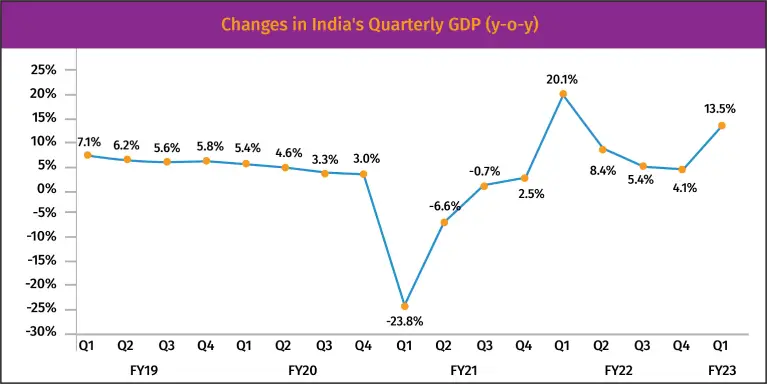

How Strong Is Economic Revival in India?

Throughout the last four fiscal years, the Indian economy has experienced many abrupt changes. Due to problems in the banking sector and a slowdown in private consumption growth, GDP growth has decreased from 8.3% in FY17 to 4% in FY20. The economic situation continued to worsen in FY21 as a result of the Covid-19 pandemic, and the Indian economy had the most severe decline of its yearly GDP, falling by 6.6%.

What happened To The Economy During And After The Epidemic?

It is important to note that the government and Reserve Bank of India (RBI) took prompt and aggressive steps to address the Covid-19 disruptions through fiscal and monetary policy measures like interest rate cuts, liquidity injections, and increased spending on health and social security. These actions may have helped to limit the economic contraction to some extent. Because to the recurrent lockdowns during pandemic waves, vulnerable businesses and households were severely harmed in terms of their finances and were given the support they needed. These prompt actions helped the economy bounce back, and the GDP increased by 8.7% in FY22 thanks to a significant base effect.

The Rebuilding Process After a Pandemic -

Global economy began to recover after the Covid-19 pandemic's three waves. Once Russia invaded Ukraine in February 2022, the dynamics of growth were, however, negatively impacted. The problem was made worse by escalating pricing pressures brought on by supply restrictions. The prospects for domestic growth were also adversely impacted by unfavourable international developments, including as tighter financial conditions, on-going supply restrictions, the protracted Russia-Ukraine war, and increased chances of a worldwide recession. A rise in inflationary issues was caused by on-going supply-side interruptions and supply-related uncertainty. In addition, there was a net decrease in capital flows, which caused the Indian rupee to weaken.

Also, the severe downside risks to the growth momentum were exacerbated by the record-level inflation of 7.28% in Q1FY23. The RBI began to reverse its lenient posture in response to growing inflationary worries and increased the key policy repo rate by 140 basis points as of May 4th, 2022. The RBI maintained its growth prediction of 7.2% for FY23 despite the additional challenge provided by the declining monetary policy support, citing the strengthening internal fundamentals and on-going resilience of the Indian economy. Also, the majority of the main international agencies have listed India's economy as one of the world's fastest-growing. The strong macroeconomic fundamentals and prompt regulatory action for preserving price stability and averting a stagflation-like situation are the key drivers of relative optimism over the domestic economy. This is clear from domestic high-frequency growth indicators, which, despite the gloomy state of the world, have been showing a slow and steady rebound thus far in FY23.

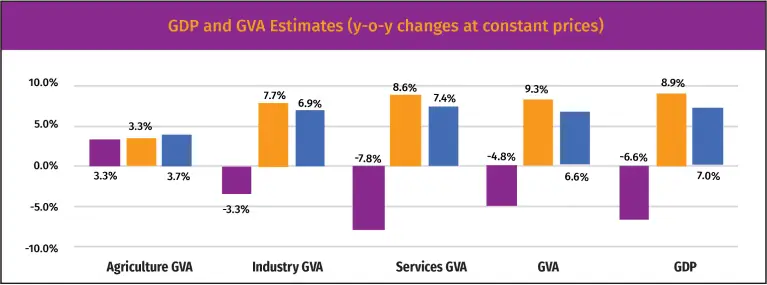

A Widespread Recovery Across All Sectors

On the supply side, steady increase in the Gross Value Added (GVA) is anticipated, notably in contact-intensive industries thanks to the anticipation of strong agricultural output and a rising service sector. Because of the challenges brought on by rising input costs and persistent supply-side disruptions, the manufacturing sector is also anticipated to contribute favourably this year.

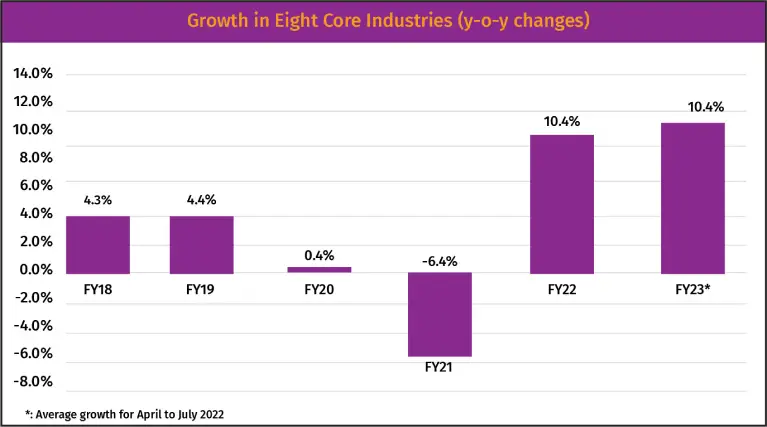

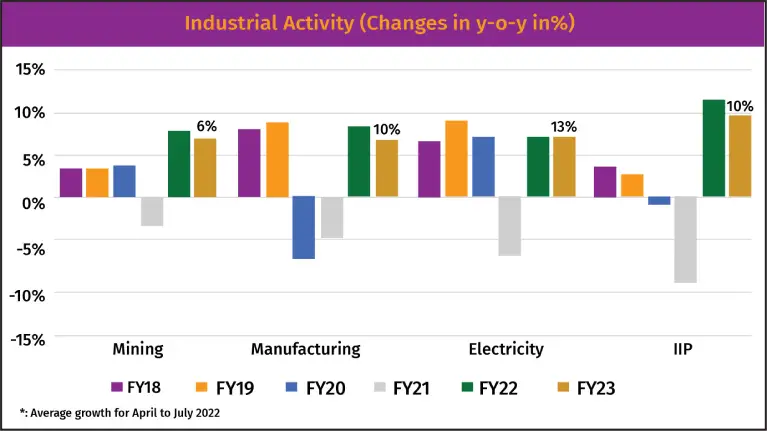

The momentum is strong and widespread according to high frequency indicators.

Eight Core Businesses Exhibiting A Significant Upswing

Concerns about inflation, which worsened in the first half of 2022 and lowered spirits, seem to have subsided recently. The increase in demand, declining input costs, and rising corporate confidence all contributed to an increase in industrial output.

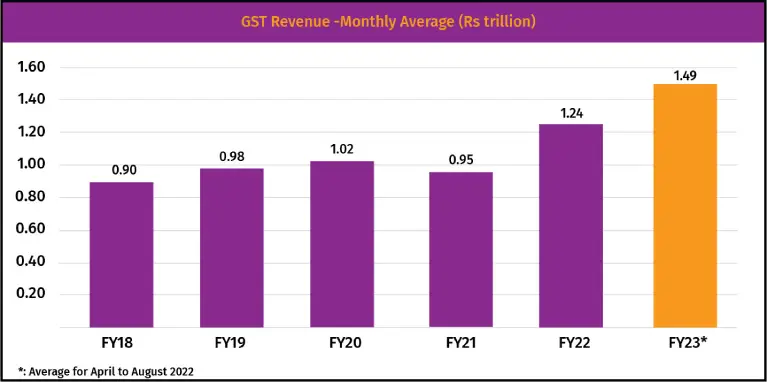

GST Monthly Receipts Demonstrate A Consistent Economic Recovery -

The consumption of taxable goods and services, represented by the gross GST revenues, increased significantly, showing increased economic activity and indications of a sustained development phase. The GST Council has taken a number of actions in the past to promote improved reporting as well as better compliance, and these actions have consistently had a favourable effect on GST collections. The technology platform needs to be stabilised in order to significantly improve tax compliance. In addition, input tax credit claims need to be monitored on time in order to further enhance tax compliance and result in higher revenue production.

Also, the GSTN was able to stabilise the technological infrastructure. Better invoice matching and the discovery of false invoices that were used to claim input tax credit have been made possible by the requirement that all firms with annual revenue over Rs. 100 crore submit electronic invoices. This has made it possible for better tax compliance and enforcement. The GSTN should eventually be able to enforce the e-invoice requirement for all enterprises with revenues exceeding Rs 10 crore, which will apply to more than 95% of taxpayers. Given these improvements, we should anticipate more revenue buoyancy, which should give us confidence to implement additional changes.

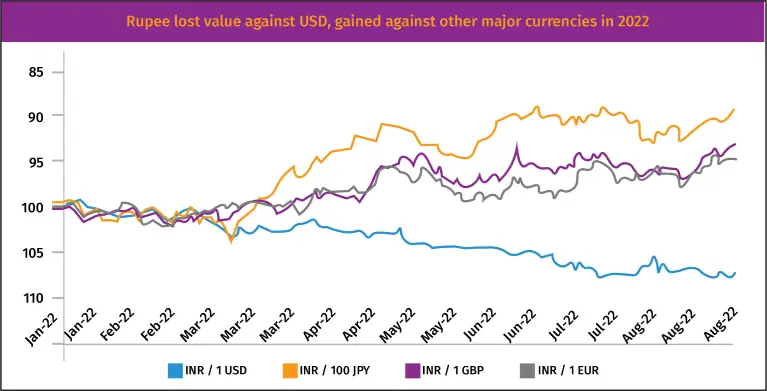

In terms of EM counterparts, the rupee has performed better in FY23 thus far. In 2022, the Indian rupee strengthened against the other major currencies despite declining against the US dollar. In contrast to the currencies of other EMEs, the Indian rupee managed to maintain relative stability versus the US dollar despite the US Fed's relentless rate hikes. The RBI's accommodating policies and successful volatility management interventions helped the Indian rupee to maintain its stability.

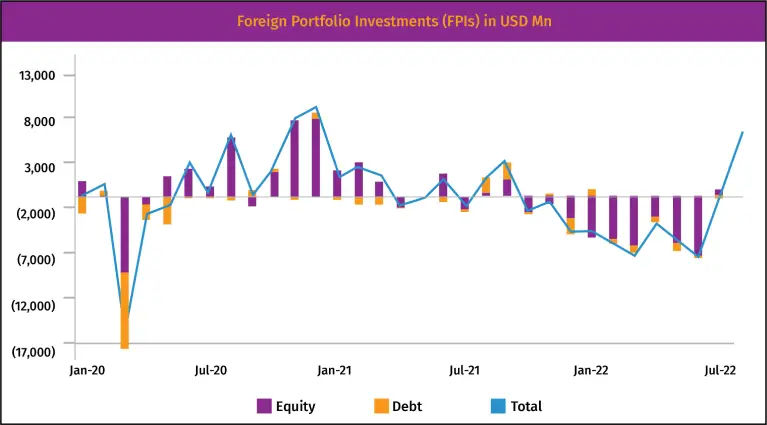

FPIs Who Have Recently Invested In Indian Equities Highlight India's Potential For Growth -

FPIs have begun to move into Indian markets in accordance with expectations of stability and growth surrounding the Indian economy, particularly in the wake of the RBI tightening interest rates.

Banking As A Core Sector -

There is a direct correlation between a healthy banking system and sustained economic expansion. After the NBFC crisis in 2019 and the Covid-19-related disruptions in 2020, there have been major changes in the banking system, mostly as a result of asset quality difficulties.

The government has invested a significant amount of capital in Public Sector Banks (PSBs) during the last 5–6 years to help them weather the NPA crisis and maintain the Basel III framework's minimum capital requirements. Before the epidemic struck, PSBs had a healthy level of capital, which put them in a better position to weather the shock of the pandemic. Following the epidemic, the RBI implemented a number of customary and novel strategies to ensure the smooth operation of the financial system. In addition to cutting key policy rates by 115 basis points (repo rates were lowered to historic lows from 5.15 to 4% levels between March and May 2020), the RBI also kept its accommodative posture throughout FY21 and FY22. The RBI also implemented a number of liquidity-boosting measures to maintain the financial system's efficiency. With the lifeblood of financing flowing, the government and RBI's concerted policy response served to lessen the pandemic's negative effects on financial markets and financial institutions.

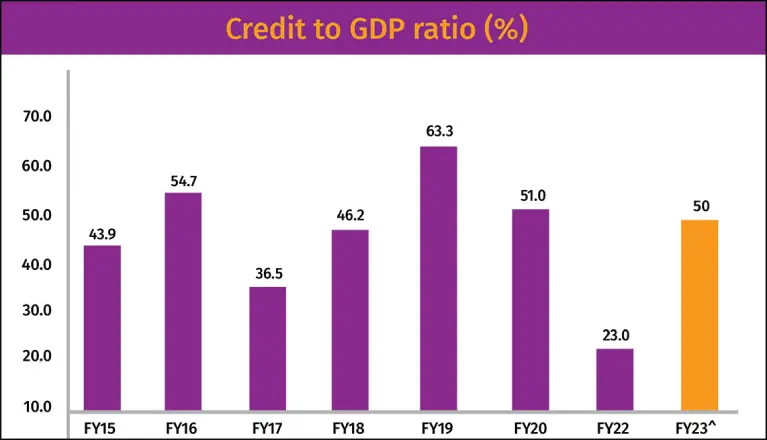

The gradual rise in the bank loan to GDP ratio is one of the most important markers of economic expansion. A lower number reveals the need for more formal credit, while a larger percentage illustrates the banking industry's proactive and active participation in the actual economy. The share of additional credit to GDP increased to as much as 63% in FY19, up from an average of 50% over the previous five years. After falling to 23% in FY22, the share is anticipated to surpass 50% in FY23.

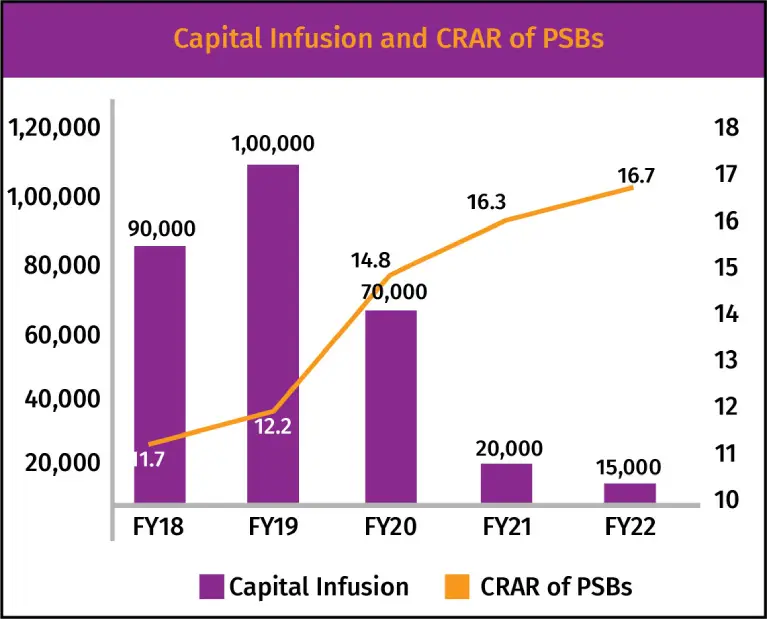

Recapitalization of Banks -

The Indian banking system was able to weather the pandemic's shock and keep its capital adequacy ratio over the Basel III framework's minimal regulatory standards. The government invested Rs 3.2 trillion in PSBs between FY17 and FY20 to assist banks in meeting the minimum capital requirement and managing sizable volumes of bad assets on their books. Its recapitalization was funded by a combination of budgetary allotment and the issuing of recapitalization bonds worth 2.76 trillion rupees. The injected funds eventually served as a buffer for the banks against potential pandemic shocks, helping to raise the Capital to Risk weighted Assets Ratio (CRAR) of PSBs from 11.7% in FY18 to 14.8% in FY20. Since March 2020, the CRAR has been increasing, reaching a new high of 16.7% in March 2022.

Bank restructuring -

In 2021, the government combined 10 PSBs into 4 banks as part of a reorganisation of the Indian banking industry. The banks now have a larger capital base, which has decreased the requirement for government capital infusion. As a result, the financial sector is now strong, with participants who are better able to absorb systemic shocks.

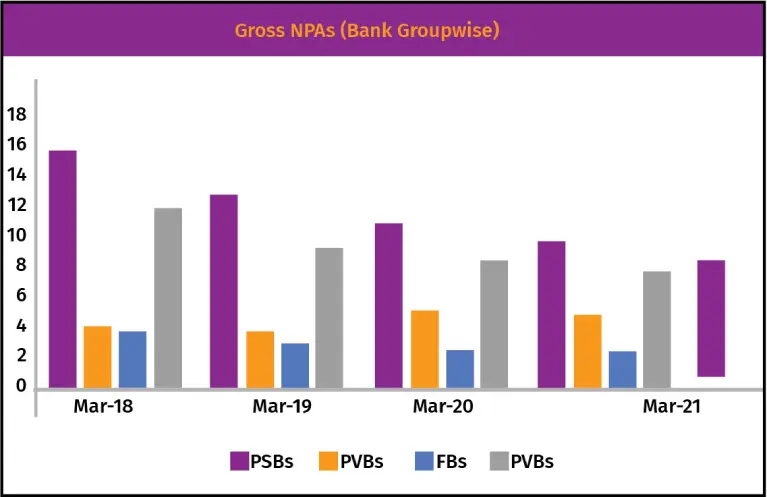

Asset Quality Ratio: Consistent growth over time

Asset quality, whose maintenance has historically been a significant concern for Indian banks, has begun to significantly improve as a result of better adherence to laws and increased government capitalization. Due to IBC-backed resolutions and write-offs, banks' asset quality improved in FY19 after hitting a low point in FY18. While banks took a cautious approach to lending and improved loan underwriting, there were also fewer new slippages to NPAs. Decreased SMA overdues and a reorganised portfolio also contributed to an improvement in asset quality and a consequent decrease in credit expenses during this time. In March 2022, the Gross Non-Performing Asset (GNPA) levels were about 5.9%, down from 11.6% in March 2018.

Credit Growth Is Accelerating More Quickly Than Anticipated -

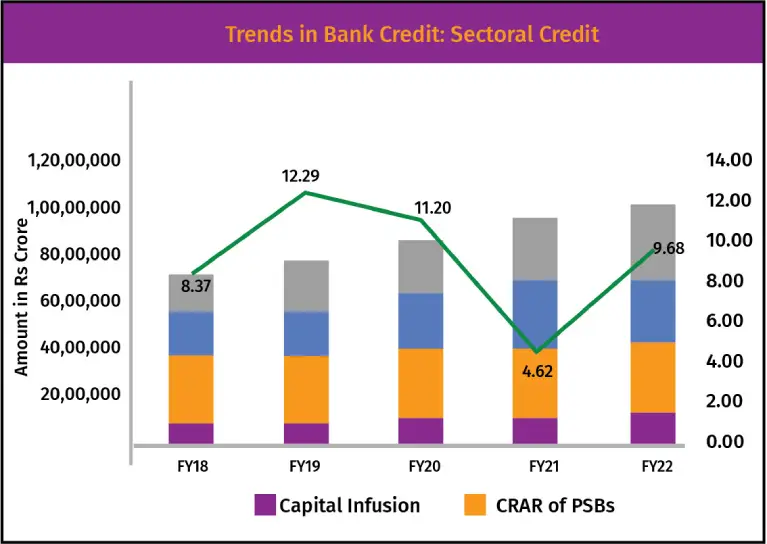

The slowdown in the economy and the stressed bank balance sheets over the past three years have kept credit growth modest, but it is now beginning to show indications of revival. It decreased to a CAGR of 10.2% from FY11 to FY20 after recording a Compound Annual Growth Rate (CAGR) of 20.9% from FY02 to FY10. Banks' risk aversion as a result of the system's historically high level of non-performing assets further hampered the flow of credit. As Covid-19 broke out, the decline in credit growth was further exacerbated by pandemic-related economic disruptions.

Given India's high development prospects and a quicker recovery in economic activity, credit growth for banks rebounded to 9.7% in FY22 and is predicted to continue buoyant or reach double digits in the following years. According to the most recent information provided by the RBI on credit outstanding, as of August 26, 2022, bank credit increased at a pace of 15.5% year over year compared to 6.1% during the same time the previous year.

The Capacity Utilisation (CU) of enterprises has also begun to show signs of improvement, which supports the idea that the economy is beginning to revive. According to data from the RBI, the CU in the manufacturing sector as a whole increased to 75.3% in Q4FY22, the highest level in the previous 12 quarters. Demand conditions have significantly improved, and businesses are increasing their stocks to accommodate incoming orders.

Strong Regulations In Place To Build a Strong Economy -

Regulators in India have a long history of being very proactive and frequently coordinate their efforts with those of the government. This has repeatedly been demonstrated by the Indian economy, which has proven resilient in the face of numerous global economic downturns and shocks. Similar to this, during the most recent period of instability (FY19-FY22), regulators and the government acted quickly with a number of structural and operational measures, giving the economy the needed boost at the time.

- Post the NBFC crisis, SEBI introduced Partial Credit Enhanced (PCE) credit ratings for NBFCs and HFCs. INDIA’S EMPLOYMENT SCENE: ARE THE GLOOMIER DAYS OVER? This enabled NBFCs and HFCs attain a better credit rating, which improved investor sentiment.

- To improve the integrity of credit ratings, SEBI also introduced tighter disclosure norms for CRAs.

- The GoI set out to amalgamate various public sector banks, which would make the resultant banks resilient, less risky and more profitable.

- Increasing the flow of credit in the economy by the lowering of the Leverage Ratio and Cash Reserve Ratio.

- Expansion and extension of its Targeted Long-Term Repo Operations.

- A special liquidity scheme for the stressed NBFC and HFC sector, as well as for Mutual Funds was introduced.

- Rs 50,000 crore relief was provided to the MSME sector.

- The Insolvency and Bankruptcy Code (Amendment) Bill, 2021, provided a pre-packed agreement for the resolution of the debt of a distressed MSME entity.

- The RBIs' Priority Sector Lending Guidelines, which included sectors like Agriculture, Education, Export Credit, Housing and MSMEs, helped stimulate lending in the economy and ensured credit availability across stressed sectors of the economy.

- The All-India Financial Institutions was refinanced to the tune of Rs 50,000 crore in FY21.

- Resolution Framework for Covid-19 Related Stress was introduced, which enabled lending institutions to formulate a resolution plan for borrowers facing stress due to Covid-19. This helped mitigate the impact of Covid-19 on borrowers and would eventually lead to the revival of the stressed sectors of the economy.

- To help relive the banks of their stressed assets, the NARCL was set-up.

- Co-operative banks were permitted to utilise the SARFAESI Act to recover bad loans.

- In view of the Punjab and Maharashtra Co-operative bank issue, the RBI was given regulatory powers over co-operative banks through the Banking Regulation (Amendment) Bill, 2021.

- At the onset of the second lockdown in FY22, the RBI launched the G-Sec Acquisition Program(G-SAP) 1.0 to provide liquidity to the system and support the yield curve during Q1FY22. The RBI launched G-SAP 2.0 for Q2FY22, which it halted in response to the easing of the lockdown, adequate liquidity and better GST collections.

- A Credit Guarantee Scheme for Micro-Financial Institutions was launched to ensure the availability of credit to small borrowers.

- The RBI increased policy rates to tackle increasing inflation with the background of rising energy prices, supply-side pressures and the easing of restrictive measures.

- The RBI also laid out stricter Credit Enhancement (CE) guidelines for Credit Rating Agencies (CRAs) to enable a common framework for better assessment of Credit Enhancement across CRAs.

- The cabinet also approved Interest Subvention for Agriculture Loans, supporting the Agriculture sector by providing it access to low-interest credit.

The Beginnings of An Economic Recovery -

India is on track to have the fastest-growing economy in the world. The Indian financial system is still thriving and stable. The Indian banking sector was able to manage the pandemic's waves and enhance their capacity for risk absorption with the help of policy support, including regulatory dispositions.

Bank credit growth showed a clear upswing in FY22 and is likely to continue with double-digit growth in FY23. Prior to slowing in FY21 due to weak business sentiments throughout the year as a result of the slowdown in the economy leading to lower demand in the market, bank credit growth showed a clear upswing in FY20.

While the industry and services sectors are both likely to raise their borrowings given the recent period's sustained improvement, credit growth in agriculture may remain constant with ongoing domestic demand. Banks have rapidly grown their proportion of retail lending over the past two years since it was a safer bet than corporate loans in terms of asset quality. Nonetheless, the demand for such credit could increase in the upcoming years due to the economy's recovery.

The regulatory environment in India has indicated proactive and prompt measures, strengthening the banking and financial services business, allowing MSMEs to survive the epidemic, and allowing NBFCs to rebound following the NBFC crisis.

As a result of the RBA's altered position on rates, there are signs that inflation may moderate from a peak of 7.8% in April 2022 to 6.71% in July 2022. Once more, this may be a precursor to India's transition to a path of steady and sustainable growth with stable prices.

Having managed the upheaval in the past few years, regulators are now focusing on adopting long-term actions to prepare the Indian economy and financial services ecosystem for a time of sustained growth. The withdrawal of the accommodative monetary policy stance to control inflation, along with policies and guidelines on Fintech, sustainable finance, and the consideration of ESG in risk assessment, show the regulators' long-term perspective, which takes into account the expected global scenario in the next 5-7 years. • The Indian economy is back on its growth path despite the global headwinds with clear indications of sustained and higher economic activity, with most sectors performing better than they did before the pandemic.

Conclusion -

Although the effects of the state of the world economy are being felt in India, the country's economy is still recovering. While local macroeconomic and financial events appear to have decoupled and showed a minor recovery, dangers to the stability of the global financial system have increased.

The financial system is still strong and helps the economy recover. The RBI and government support have helped the Indian banking system successfully resist the pandemic's negative effects. A favourable regulatory environment and a sizeable infusion of capital have helped absorb the shocks and laid the groundwork for banks to successfully respond to the now apparent increased demand for loans. Indicating long-term stability in the financial system, both banks and non-banking entities have enough capital buffers to weather future adversities. In addition, banks have strengthened their capital and liquidity situations as asset quality has increased.

While ensuring macroeconomic and financial stability, regulatory efforts are still being made to strengthen the financial system against unanticipated negative events and to enhance the lending climate to promote recovery. The rise of bank credit is already in double digits and is increasing up pace.

There is a definite sign that regulators are cognizant of what the financial sector and economy as a whole will need in the future. With futuristic policies like central bank digital currency and the taxation of virtual digital assets, together with a supportive position on digital banking, regulators are guiding the Indian financial system towards the adoption of novel financial technologies.

The regulators are also mindful of India's environmental and sustainability compliance goals. As a result, the RBI and SEBI have begun to consult with financial system stakeholders in order to develop appropriate regulations for Environmental, Social, and Governance (ESG) disclosures and risk assessment.

India is now firmly on the cusp of long-term progress towards global economic leadership due to the combination of a strong domestic financial system, sensitive regulatory control, and early indicators of a quicker rebounding economy.